Many temple administrators, trust leaders, and donors struggle with the problem of unclear donation laws in India. Temple trusts need funds to operate, devotees want to contribute, but both often find tax and legal rules confusing. This can agitate concerns: Will the donations be used properly? Can donors claim tax benefits? Could non-compliance trigger penalties? The good news is there’s a solution: a clear understanding of the donation laws (especially Sections 12A, 80G and FCRA) can ensure legal compliance for religious trusts and satisfied donors.

This guide, Legal Aspects of Religious Donations in India, uses facts and government guidance to answer these questions for temples (e.g. Hanuman, Kedarnath, Tirupati Balaji) and NGOs.

What Counts as a Religious Donation in India?

A “religious donation” in India typically means a voluntary gift (usually money or valuables) given to a temple, church, mosque or religious trust without any quid-pro-quo. Legally, the Income Tax Act only recognizes donations to approved institutions or funds for tax benefits.

For example, gifts to approved temples or a charitable society (registered under Section 12A) qualify, but paying for temple services or offerings does not. In practice, only monetary donations to authorized religious trusts count as tax-deductible “donations”. Non-cash gifts (food, clothes, etc.) are usually not eligible. The temple or trust must be notified by the government (e.g. via a gazette notification under Section 80G) as a place of worship of renown.

In short, donating ₹500 to a temple account with a proper receipt is a “religious donation”; buying a pooja item or giving an idol to the temple normally is not recognized under law. Always check that the trust’s PAN and registration number are on the donation receipt. For more on donation law in India, see our charity law overview.

Why Understanding the Legal Aspects of Religious Donations in India Is Crucial Today

In today’s regulatory environment, being aware of the legal aspects of religious donations in India is no longer optional—it’s essential for every religious institution. Whether you’re managing a centuries-old Hanuman temple or setting up a new Christian trust or mosque committee, the compliance landscape is tightening. Institutions that fail to grasp the legal aspects of religious donations in India risk losing credibility, tax exemptions, and donor support.

One of the most common issues revolves around the 80G deduction for temple donations. Devotees often contribute in good faith, expecting a tax break. But if the institution isn’t registered under Section 12A and 80G registration, those donations become ineligible. This is especially critical for new religious trusts, which must actively pursue these certifications to provide tax exemption for religious donations and remain compliant.

Foreign donations present another layer of responsibility. Many institutions are unaware of how strict the FCRA for religious trusts has become. From submission of donor identity records to quarterly financial disclosures, the FCRA for religious trusts requires meticulous attention. Non-compliance not only results in penalties but can also lead to a permanent ban on foreign contributions—a blow for institutions that rely on international devotees.

Moreover, a surprisingly large number of people still do not know how to donate to temple legally. They might give cash above ₹2,000 or donate to institutions lacking proper registration. This makes it imperative for religious leaders to educate their followers on how to donate to temple legally while also tightening internal procedures.

Whether you’re seeking tax exemption for religious donations, ensuring your trust has valid Section 12A and 80G registration, or working to stay on the right side of FCRA for religious trusts, these steps are non-negotiable. Following the legal aspects of religious donations in India ensures not just legality, but also builds trust, accountability, and long-term sustainability for religious institutions.

Legal Aspects of Religious Donations in India: 80G Deduction for Temple Donations

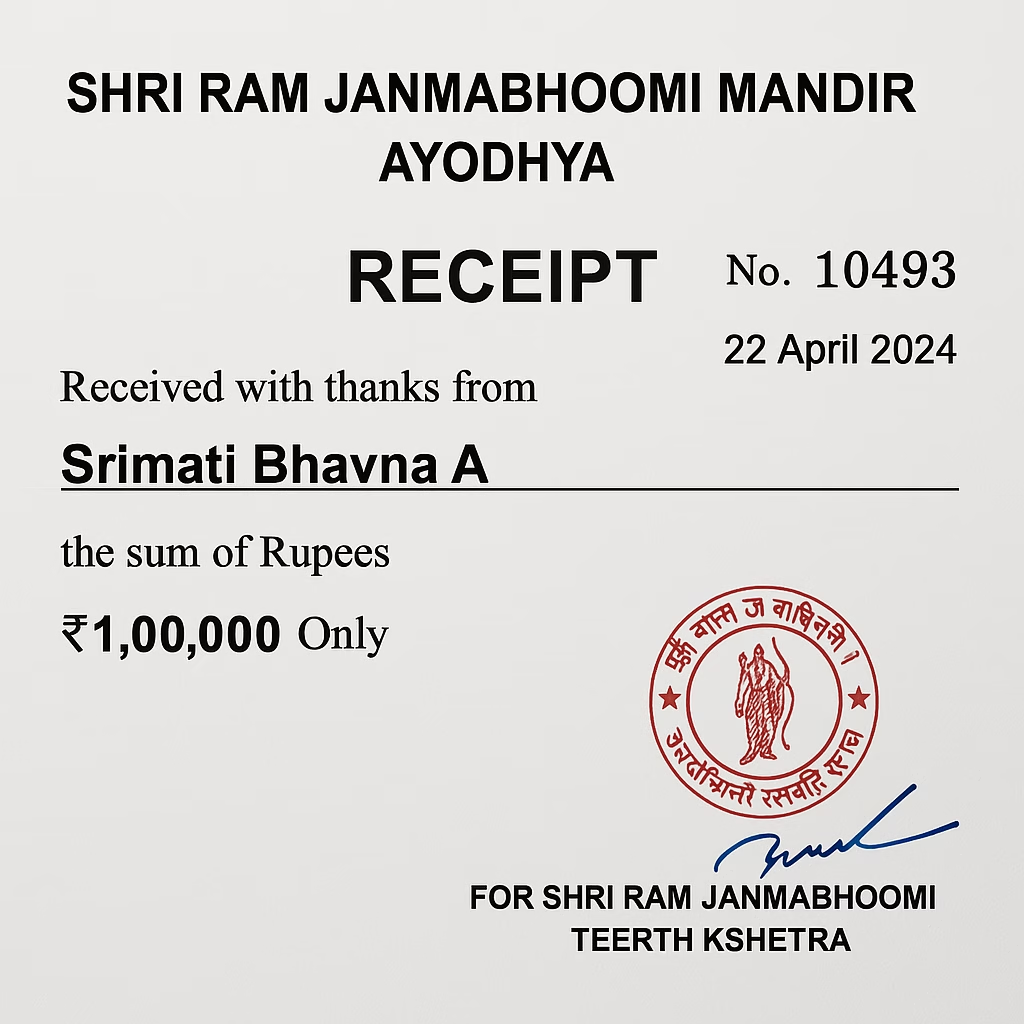

The biggest incentive for donors is the 80G deduction for temple donations. Under Section 80G of the Income Tax Act, 50% of eligible donations can be deducted from the donor’s taxable income (with some donations qualifying for 100% subject to caps). Temples and trusts must themselves register under Section 80G for donors to claim this benefit. For instance, the Tirumala Tirupati Devasthanams (Balaji Temple) issues an “Income Tax Exemption Certificate under 80G 50%” to donors. Similarly, contributions to the Ayodhya Ram Mandir Trust qualify for a 50% deduction.

Key points: Donors should pay by cheque, electronic transfer or cash below ₹2,000 (cash over ₹2,000 is ineligible). Always get a stamped receipt showing your name, PAN, trust’s name and 80G registration number. Note that deductions apply only if the trust is approved (e.g. in 2024-25, donations for renovating the Kedarnath or Ram temples are tax-deductible).

The total deductible donations are capped (generally 10% of the donor’s adjusted gross income). If a temple offers puja kits or prasadam in return, treat those as purchases, not donations. In short, donors saving tax should ensure the temple trust has valid 80G certification and that they obtain proper receipts. (Learn more: see our 80G donation guide.)

FCRA Rules for Foreign Donations to Indian Religious Trusts

Receiving money from abroad adds another layer: the Foreign Contribution (Regulation) Act (FCRA) applies. Any foreign donation to a religious trust (e.g. Hindu temple society, Christian church, Sikh gurudwara) requires FCRA compliance. As per the Ministry of Home Affairs, a person or organization with a cultural, educational or religious program can only accept foreign contributions after obtaining prior permission or registration under FCRA.

This means an Indian temple trust must register with MHA’s FCRA Division before accepting funds from foreigners or NRIs (donations by NRIs from their own savings aren’t treated as “foreign contribution”, but best practice is to use normal banking channels).

All foreign funds must be deposited into a dedicated FCRA-designated bank account – no mixing with domestic funds. Violating FCRA (like accepting foreign cash or using it for banned activities) can invite heavy penalties. In practice, leading religious trusts (e.g. ISKCON, TTD, Shrine Boards) follow these rules strictly. If your trust plans to fundraise internationally, review the FCRA FAQs or consult our FCRA compliance guide.

Section 12A & 80G: Legal Setup for Hanuman Temples and Trusts

Proper setup is crucial. Any temple trust (Hanuman, Shiva, Krishna, etc.) should register under Section 12A of the Income Tax Act to claim tax exemptions on its own income. Without 12A/12AB registration, the trust’s earnings (donations, interest) are fully taxable. Second, to pass benefits to donors, the trust must also get 80G registration.

A trust that only has 12A (exempt status) but not 80G cannot offer 80G certificates to donors. Conversely, 80G registration does not waive the trust’s income tax unless 12A is also there. For example, the government’s official notification lists many temple trusts (including a “Sri Anjaneyaswami” – i.e. Lord Hanuman – in Tirumala) as places of worship eligible under 80G.

This shows that a Hanuman temple trust in that group can give donors a 50% deduction. In practice, trustees must apply online (via Form 10A/10AB) for 12A/12AB within the prescribed timeline and renew every 5 years, and separately apply for 80G registration. Only then will donations to Shri Hanuman Mandir or similar shrines qualify for tax breaks. (For details on registering, see the tax department’s NGO portal and our post on Section 12A and 80G registration.)

Common Legal Mistakes Devotees Make While Donating

Even pious donors can err. One frequent mistake is donating in cash above the legal limit – 80G deductions are only allowed for cash gifts up to ₹2,000 . A ₹5,000 cash offering at the temple will NOT fetch any tax benefit. Donors also often forget to obtain proper receipts.

As per tax rules, valid receipts must list the donor’s PAN, the trust’s registration number, and the exact donation amount . No receipt (or one lacking these details) means you can’t claim 80G even if the trust is eligible.

Giving gifts in kind (like food, clothes, or holy items) is another pitfall – these are not “donations” for tax purposes . Devotees sometimes “spread” their offerings (e.g. donating ₹2,001 hoping to claim ₹1 as tax break) or donate through unofficial middlemen; these can violate tax laws. Foreign devotees sending money should avoid informal channels (use official donation links or banking remittances).

Finally, donating to an unregistered NGO or unknown handler hoping it will reach a temple can backfire; always verify the entity’s 12A/80G and FCRA status. In summary, check the trust’s credentials, donate above ₹2,000 via cheque/online if you want tax benefit, insist on a proper 80G receipt, and never hand over cash or valuables without documentation.

Great, I’ll now expand the blog by adding a new section covering the impact of non-compliance with donation laws in India, including examples involving major temples like Tirupati and Kedarnath. I’ll also include real-world legal or administrative consequences to provide depth. I’ll let you know as soon as it’s ready.

Consequences of Non-Compliance for Temple Trusts and Devotees

A donor offers a coin in this illustrative image. Religious trusts in India must meet strict legal requirements on donations. Under the Income Tax Act, a temple must register its trust (Section 12A/12AB) to be tax-exempt on its income and secure Section 80G approval so donors can claim deductions. Failure here is costly: without 12A, a trust “will then be required to pay taxes like any other non-exempt entity”.

Likewise, without 80G approval, donors lose tax benefits altogether. This can discourage giving and erode public goodwill. For instance, the Union Budget 2025 noted that “only if the trust is [80G] approved can donors get a tax benefit”. In short, a temple that misses these registrations not only loses exemptions on its own earnings but also forces devotees to forego deductions, reducing the incentive to donate.

A collection jar filled with coins – symbolising temple offerings or foreign donations. Foreign contributions are governed by the FCRA, and lapses are heavily penalised. Even “technical discrepancies” can trigger action. In Tirumala Tirupati Devasthanams (TTD) – one of India’s richest temple trusts – the Home Ministry found its annual FCRA returns in an “incorrect format” and fined it ₹3.19 crore.

As a result, TTD’s FCRA licence has been kept in abeyance for three years, meaning it cannot legally receive or even bank foreign “hundi” donations. Over a year, nearly ₹27 crore in foreign currency offerings piled up undeposited because SBI refused deposits without donor details. In effect, a technical filing mistake froze millions of rupees of devotions. Across India, the Home Ministry has cancelled FCRA registrations of NGOs for “violation” – warning that cancelled organisations “will no longer be able to receive foreign contributions nor utilise existing funds”. This underscores that a temple trust’s failure to comply can abruptly halt its foreign fundraising, stalling major pilgrim-funded projects.

Legally and reputationally, mishandling donation laws also hurts public trust. For example, the Badrinath-Kedarnath Temple Committee recently discovered scammers installing fake QR-code donation boards at the Kedarnath and Badrinath shrines. The committee lodged an FIR and warned devotees not to scan unapproved donation links, fearing such frauds could misdirect offerings and “tarnish the reputation of the temples”. Similarly, if devotees learn that a temple is under audit, facing fines, or has lost its tax-exempt status, they may hesitate to give. Lack of compliance can spark legal disputes or public scrutiny, forcing trust officials to divert resources into court battles or corrective measures instead of spiritual service.

Key Risks & Impacts:

- Loss of Tax Exemption: A temple without valid 12A/12AB registration must pay regular taxes on income. Even minor form errors no longer excuse deregistration (new rules grant leniency), but failure to revalidate 12A means forfeiture of exemption.

- Donor Disincentives: Without 80G approval, donations cannot be claimed as tax-deductible. Donors may reduce gifts if they lose these benefits, cutting the temple’s funding.

- FCRA Suspension/Cancellation: Non-compliance (even unintentional) can suspend or cancel a temple’s foreign donation licence. The TTD case shows how quickly penalties can accumulate, and other NGOs have had FCRA licences revoked, freezing their funds. This blocks contributions from NRIs and foreign pilgrims.

- Government Audits & Penalties: Irregular accounts or nondisclosures invite Income Tax and CAG audits. Penalties can include heavy fines or demands to deposit unjust withdrawals (often many times the benefit).

- Legal & Reputational Fallout: Unauthorised solicitations (like the Kedarnath QR scam) or discovered misuse leads to FIRs or media reports. Legal fights over donations can embroil the temple and discourage devotees. Loss of donor confidence is hard to recover.

In sum, legal compliance for religious trusts is non-negotiable. Temples must keep registrations current and follow FCRA rules to protect themselves and their devotees. Doing so ensures that donations continue flow tax-free to worthy causes, rather than getting tied up in penalties or fraud. By meeting all statutory requirements – from transparent accounts to timely filings – temple authorities safeguard the trust placed in them by generations of devotees.

Sources: Current Indian legal and news reports on temple trusts and NGOs.

Hindu, Muslim, and Christian Religious Donations: A Legal Comparison

In the context of the legal aspects of religious donations in India, understanding the regulatory differences across Hindu, Muslim, and Christian religious institutions is essential for ensuring legal compliance for religious trusts. Each religious body must navigate compliance under the Income Tax Act and the Foreign Contribution Regulation Act (FCRA), especially to avail tax exemption for religious donations and remain eligible for the 80G deduction for temple donations. This applies not just to Hindu temples but also to Muslim mosques and Christian churches, each functioning under different legal structures. The process also requires awareness of how to donate to temple legally, which varies across religions depending on their governing frameworks.

Hindu Temples and Trust Donations

Hindu religious donations are often managed by temple trusts or boards under state laws like Tamil Nadu’s HR&CE Act or Andhra Pradesh’s TTD Act. Major institutions like the Tirumala Tirupati Devasthanams (TTD) or Ram Janmabhoomi Trust attract vast donations annually. To maintain the legal aspects of religious donations in India, these trusts must be registered under Section 12A and 80G registration.

This ensures that donors can receive the 80G deduction for temple donations, which provides a 50% income tax benefit. It also fulfills legal compliance for religious trusts and protects the temple’s income from taxation. For example, in 2025, Banke Bihari Temple secured FCRA clearance, highlighting how seriously temples are now pursuing global donor compliance under the FCRA for religious trusts.

The registration under Section 12A and 80G registration enables the temple to extend tax exemption for religious donations to its devotees, reinforcing the core legal aspects of religious donations in India. Without this compliance, neither the trust nor the devotee benefits financially. For foreign donations, temples must maintain an FCRA-designated bank account and comply with quarterly disclosures, as outlined in the FCRA for religious trusts. For any devotee wondering how to donate to temple legally, this includes verifying the trust’s legal certifications before making a contribution.

Muslim Donations and Waqf Endowments

Muslim donations are primarily managed through waqf properties under the Wakf Act, 1995. Each state has a Waqf Board responsible for handling donations made to mosques and madrassas. Like Hindu temples, Muslim religious bodies must comply with the legal aspects of religious donations in India by obtaining Section 12A and 80G registration to issue tax-deductible receipts. When eligible, donors receive tax exemption for religious donations and benefit from the 80G deduction for temple donations—which, in this context, applies to mosque donations.

Institutions such as the Jama Masjid Delhi are eligible to be registered and compliant with FCRA for religious trusts for foreign contributions. While waqf boards are statutory bodies, the law still mandates documentation and financial reporting under FCRA guidelines. Maintaining legal compliance for religious trusts is key to their functioning. Understanding how to donate to temple legally, even within Islamic traditions, involves ensuring contributions are routed through verified and registered waqf channels.

Christian Churches and Charitable Trusts

Christian organizations operate under diocesan trusts or registered societies such as the Church of North India or the Catholic Bishop’s Conference of India. These bodies must also adhere to the legal aspects of religious donations in India, including Section 12A and 80G registration, to allow donors to claim the 80G deduction for temple donations. While these donations support different faith-based activities, the financial compliance under Indian law remains the same.

Churches and Christian institutions often maintain FCRA licenses to receive international missionary and charitable donations. This means they are deeply enmeshed in the FCRA for religious trusts framework, and any lapses could result in frozen accounts or legal action. Institutions that fail to maintain legal compliance for religious trusts may lose eligibility for tax exemption for religious donations, affecting operations and donor trust. Educating donors on how to donate to temple legally—or in this case, to a church or mission—ensures lawful and effective philanthropy.

In conclusion, while the modes of worship and donation vary across religions, the legal aspects of religious donations in India require uniform attention to registration, tax exemption, and FCRA compliance. Whether it’s claiming the 80G deduction for temple donations, filing for Section 12A and 80G registration, complying with FCRA for religious trusts, or helping devotees understand how to donate to temple legally, all religious organizations must strive for airtight legal integrity. Ensuring tax exemption for religious donations across Hindu, Muslim, and Christian institutions not only fosters trust but protects the sanctity and sustainability of India’s diverse religious heritage.

Final Thoughts on Religious Donation Compliance in India

Navigating the legal aspects of religious donations in India is crucial for every religious institution—whether it is a Hindu temple, a mosque, or a church. By ensuring proper Section 12A and 80G registration, institutions can protect their income and help donors receive legitimate tax exemption for religious donations. Failure to comply not only results in financial penalties but can also erode public trust.

Understanding and maintaining legal compliance for religious trusts involves more than just filing paperwork. It demands awareness of evolving laws, particularly those governing the FCRA for religious trusts, which is essential for any organization accepting foreign contributions. Religious leaders must also take active steps to educate followers on how to donate to temple legally, ensuring that their devotion translates into lawful support.

Across faiths, claiming the 80G deduction for temple donations offers a tangible benefit to donors while reinforcing accountability in religious giving. When devotees know how to donate to temple legally, and when institutions honor that trust through full compliance, the entire ecosystem of religious giving in India becomes more transparent, secure, and sustainable.

By focusing on the legal aspects of religious donations in India, ensuring tax exemption for religious donations, managing FCRA for religious trusts properly, and maintaining up-to-date Section 12A and 80G registration, we pave the way for responsible spirituality. Let every contribution—whether to a Hanuman temple, a mosque, or a Christian mission—be both an act of faith and an example of legal integrity.

This article is intended for informational purposes only. HanumanStories.com does not provide legal advice and is not responsible for any decisions made based on the content presented herein. Please consult a qualified legal professional for specific advice related to religious donations, tax exemptions, and compliance with Indian law.

Sources: Authoritative government and financial sources (Income Tax Act sections, MHA FCRA FAQs, TTD official info) are cited above for accuracy.

References and Source Acknowledgment

To ensure this article reflects the most accurate and legally sound information on the legal aspects of religious donations in India, data was compiled from official government portals, statutory guidelines, and reputable Indian news outlets. These sources were chosen specifically for their authority on topics like Section 12A and 80G registration, tax exemption for religious donations, FCRA for religious trusts, and procedures on how to donate to temple legally. Below is a list of the primary references consulted in the preparation of this blog:

Official and Reputed Sources:

- Income Tax Department of India – Guidelines on Section 12A, 12AB, and 80G registration

https://www.incometaxindia.gov.in - Ministry of Home Affairs (MHA), Government of India – FCRA registration rules and compliance instructions

https://www.mha.gov.in - Central Waqf Council – Legal framework for Waqf Boards and management of Islamic endowments

https://centralwaqfcouncil.gov.in - Economic Times – Report on TTD FCRA compliance and penalty case

https://economictimes.indiatimes.com - Press Information Bureau (PIB) – Updates on Ram Janmabhoomi and Indo-Islamic Cultural Foundation trust recognition

https://pib.gov.in - LiveLaw / Bar & Bench – Tax rulings related to religious trusts and charitable institutions

- The Hindu / Indian Express – Articles detailing the FCRA status of Church of North India, Banke Bihari Temple, and other trusts

These sources have been used to validate claims, support examples, and illustrate the practical implementation of donation laws across different religious communities.

If you’re interested in how ancient traditions intersect with modern spiritual practice, don’t miss our detailed post on Ayurvedic Practices from the Ramayana. It offers timeless health wisdom inspired by the same cultural and devotional roots that guide the legal and ethical framework of religious donations in India.

1 thought on “6 Legal Aspects of Religious Donations in India You Need to Know”